Healthcare expenses are increasing rapidly, and serious illnesses can create both emotional and financial challenges for families. Diseases such as cancer, heart attack, stroke, kidney failure, and major organ transplants often require expensive treatments that can quickly exhaust savings. This is where Critical Illness Insurance becomes an important financial safety tool.

Unlike regular health insurance, Critical Illness Insurance provides a lump-sum payout upon the diagnosis of a covered critical illness. This amount can be used for medical treatment, household expenses, loan repayments, or any other financial needs during recovery.

In this comprehensive guide, we will discuss everything about Critical Illness Insurance, including its benefits, coverage, eligibility, exclusions, and how to choose the best plan.

What Is Critical Illness Insurance?

Critical Illness Insurance is a specialized insurance policy that provides financial protection against severe and life-threatening diseases.

When the insured person is diagnosed with a covered critical illness and meets the policy conditions, the insurance company pays a predetermined lump-sum amount.

The policyholder can use this money as needed without restrictions.

Why Critical Illness Insurance Is Important

Modern lifestyles have increased the risk of major health conditions.

Common reasons people buy Critical Illness Insurance include:

- Rising healthcare costs

- Increasing lifestyle diseases

- Financial security during treatment

- Income replacement during recovery

- Protection of family savings

A critical illness can affect not only health but also long-term financial stability.

How Critical Illness Insurance Works

The process is simple:

Step 1: Purchase a Policy

Choose a coverage amount based on your financial needs.

Step 2: Pay Premiums

Regular premiums keep the policy active.

Step 3: Diagnosis of Covered Illness

If a covered illness is diagnosed and policy conditions are met, a claim can be submitted.

Step 4: Claim Verification

The insurance company reviews medical records and supporting documents.

Step 5: Lump-Sum Payment

Once approved, the insurer pays the insured amount directly to the policyholder.

This payout is generally independent of actual treatment expenses.

Benefits of Critical Illness Insurance

1. Financial Protection

One of the biggest advantages of Critical Illness Insurance is financial security during difficult times.

The lump-sum benefit helps cover:

- Medical expenses

- Rehabilitation costs

- Home care expenses

- Travel for treatment

2. Income Replacement

Serious illnesses often force people to stop working temporarily.

Insurance benefits can help replace lost income.

3. Protection of Savings

Medical treatment can quickly deplete savings.

Critical illness coverage helps preserve financial resources.

4. Flexibility of Usage

Unlike traditional health insurance, policyholders can use the payout for any purpose.

5. Peace of Mind

Knowing that financial support is available can reduce stress during recovery.

Diseases Covered Under Critical Illness Insurance

Coverage varies by insurer, but many policies include:

Cancer

Many plans cover major forms of cancer.

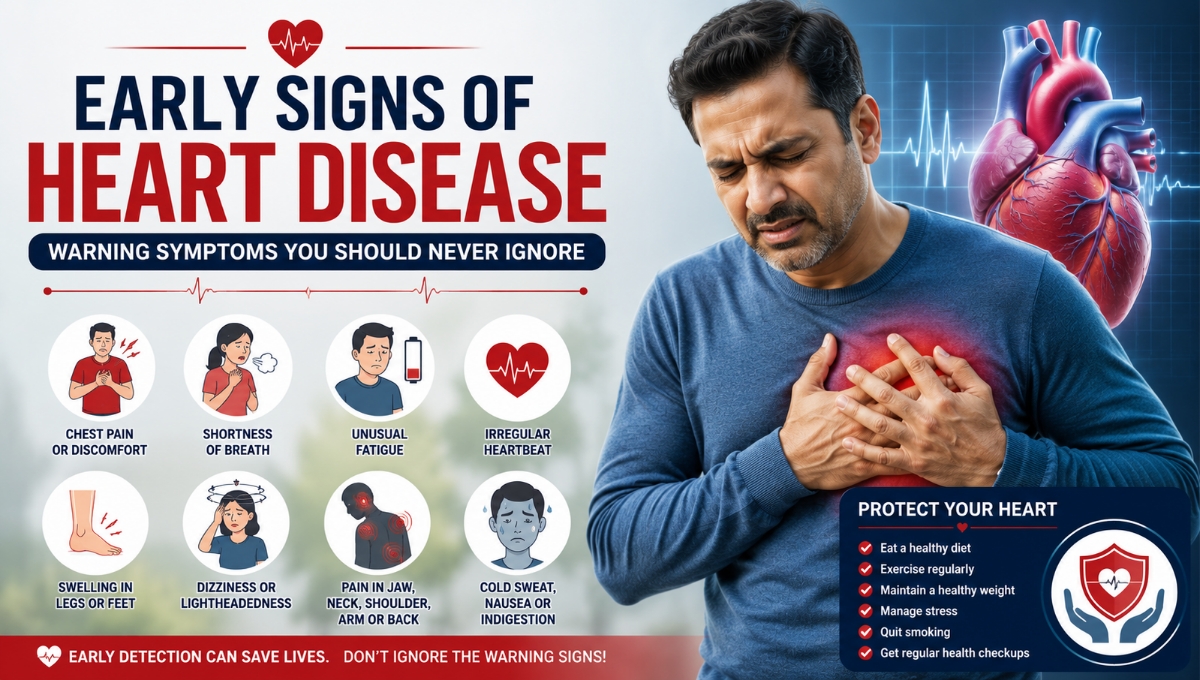

Heart Attack

One of the most commonly covered critical illnesses.

Stroke

Coverage may include strokes resulting in permanent neurological damage.

Kidney Failure

End-stage renal failure requiring regular dialysis is often covered.

Major Organ Transplant

Coverage may include heart, liver, lung, or kidney transplants.

Coronary Artery Bypass Surgery

Many policies include major heart surgeries.

Paralysis

Permanent paralysis may qualify for benefits.

Multiple Sclerosis

Certain policies provide coverage for severe neurological conditions.

Who Should Buy Critical Illness Insurance?

Almost everyone can benefit from Critical Illness Insurance, especially:

- Working professionals

- Self-employed individuals

- Parents with dependents

- Individuals with family history of critical diseases

- Sole income earners

- Business owners

Financial protection becomes increasingly important with age and responsibilities.

Difference Between Health Insurance and Critical Illness Insurance

Health Insurance

- Covers hospitalization expenses

- Pays medical bills

- Often offers cashless treatment

- Reimburses eligible expenses

Critical Illness Insurance

- Pays a fixed lump-sum amount

- Can be used for any purpose

- Provides income support

- Helps manage non-medical expenses

Many financial experts recommend having both types of coverage.

Factors Affecting Critical Illness Insurance Premiums

Age

Premiums generally increase with age.

Health Condition

Existing medical conditions may affect pricing.

Coverage Amount

Higher coverage leads to higher premiums.

Lifestyle Habits

Smoking and certain health risks may increase costs.

Policy Features

Additional benefits may affect premium rates.

How Much Coverage Should You Choose?

Choosing the right coverage depends on:

- Current income

- Family responsibilities

- Existing savings

- Outstanding loans

- Healthcare costs

Many experts recommend coverage that can support several years of financial obligations.

Common Exclusions in Critical Illness Insurance

While policies provide extensive coverage, certain situations may not be covered.

Common exclusions include:

- Pre-existing conditions (within specified limits)

- Self-inflicted injuries

- Certain waiting-period illnesses

- Non-covered diseases

- Fraudulent claims

Always review policy documents carefully before purchasing.

Waiting Period in Critical Illness Insurance

Most policies include a waiting period.

This means coverage begins only after a specified duration from policy purchase.

Waiting periods vary between insurers.

Survival Period Explained

Many Critical Illness Insurance plans require the insured person to survive for a specified number of days after diagnosis.

This is known as the survival period.

The exact duration varies depending on the policy.

Advantages of Buying Critical Illness Insurance Early

Purchasing insurance at a younger age offers several benefits:

- Lower premiums

- Better coverage options

- Easier approval

- Longer protection period

- Reduced risk of exclusions

Early planning can significantly reduce long-term costs.

How to Choose the Best Critical Illness Insurance Plan

Compare Coverage

Review the list of covered illnesses.

Check Claim Settlement Ratio

Choose insurers with strong claim settlement records.

Understand Policy Terms

Carefully review exclusions, waiting periods, and survival periods.

Evaluate Coverage Amount

Select coverage that matches your financial responsibilities.

Compare Premiums

Look for value rather than simply choosing the cheapest plan.

Common Mistakes to Avoid

Choosing Insufficient Coverage

Low coverage may not provide adequate financial protection.

Ignoring Policy Conditions

Always understand waiting periods and exclusions.

Buying Coverage Too Late

Premiums increase with age and health risks.

Not Comparing Plans

Different insurers offer varying benefits and features.

Future of Critical Illness Insurance

The insurance industry continues to evolve.

Emerging trends include:

- Digital policy management

- Faster claim processing

- Personalized coverage options

- Online policy comparison

- AI-based underwriting

These innovations are making insurance more accessible and efficient.

Conclusion

Critical Illness Insurance is an essential financial protection tool that helps individuals and families manage the financial impact of serious illnesses. With rising healthcare costs and increasing lifestyle-related diseases, having adequate coverage can provide much-needed support during challenging times.

Whether you are a young professional, a business owner, or the primary earner in your family, investing in Critical Illness Insurance can protect your savings, replace lost income, and provide peace of mind. By choosing the right policy and sufficient coverage, you can secure your financial future against unexpected health challenges.

Also Read

Healthy Lifestyle Habits for Beginners: A Complete Guide to Living a Healthier Life

Best Natural Remedies for Good Health: Simple Ways to Stay Healthy Naturally